The Rise of China in ADC Development

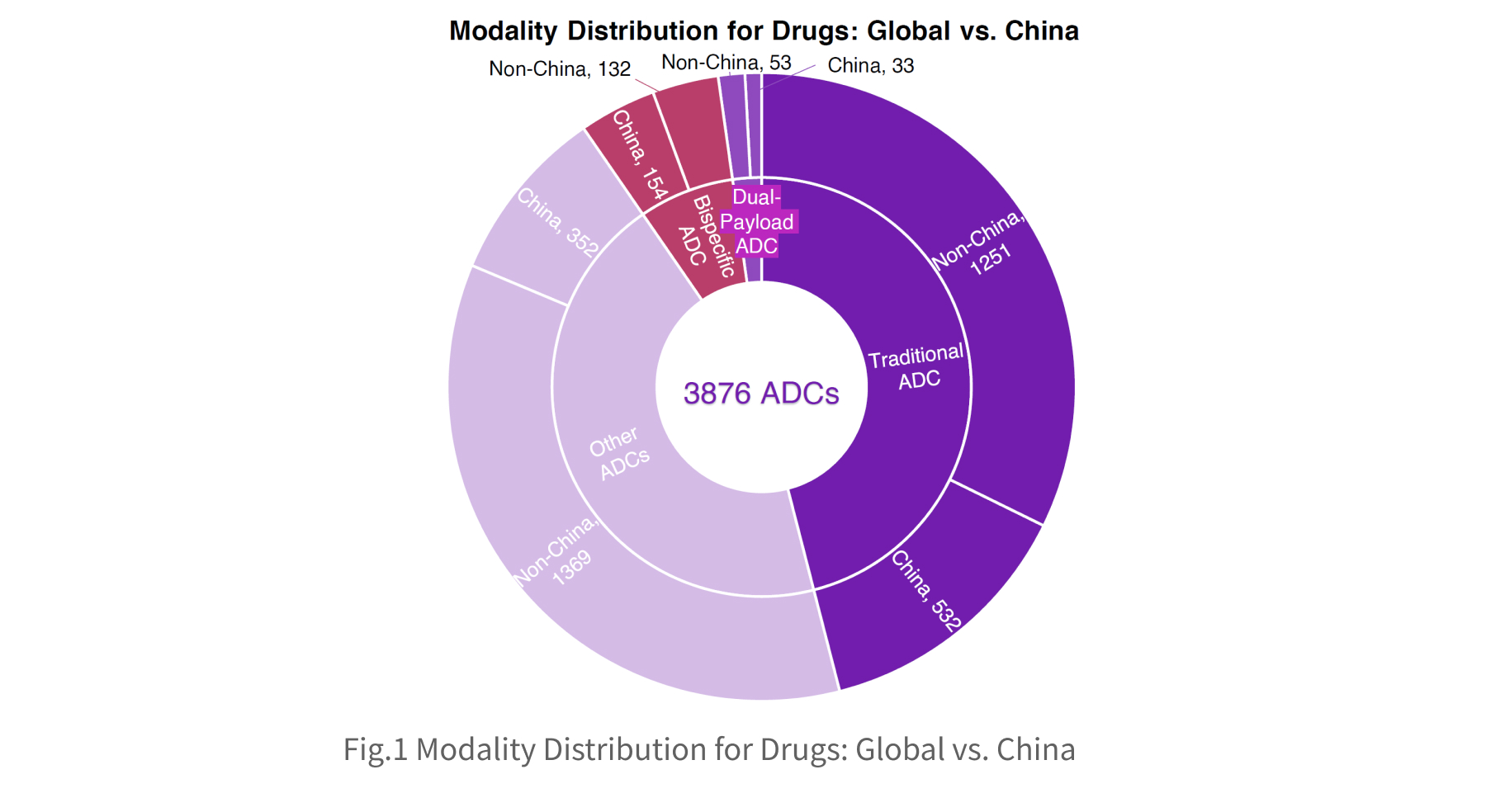

Across the global ADC landscape, traditional, bispecific, and dual-payload ADCs comprise more than half of all assets. China’s participation is substantial, accounting for 25% of all assets in these categories, with an especially strong presence in next-generation modalities: 54% of bispecific ADCs and 38% of dual-payload ADCs involve Chinese developers.

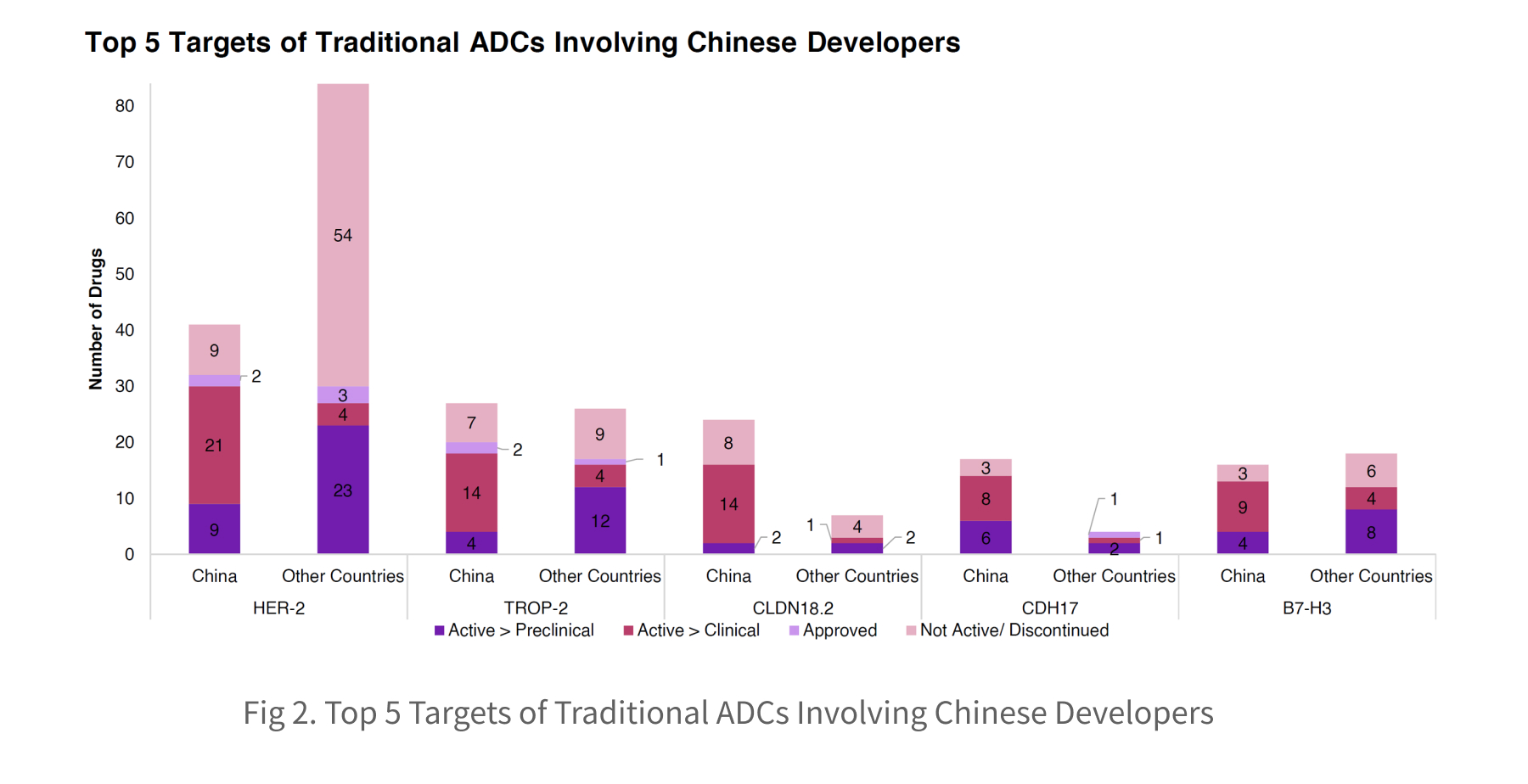

Within traditional ADC programs involving China-based companies, HER2 and TROP-2 remain the dominant targets, closely aligned with global development patterns. Rather than simply joining a global bandwagon, Chinese developers demonstrate strong strengths in advancing targets that receive comparatively limited attention from other developers, such as CLDN18.2 and CDH17.

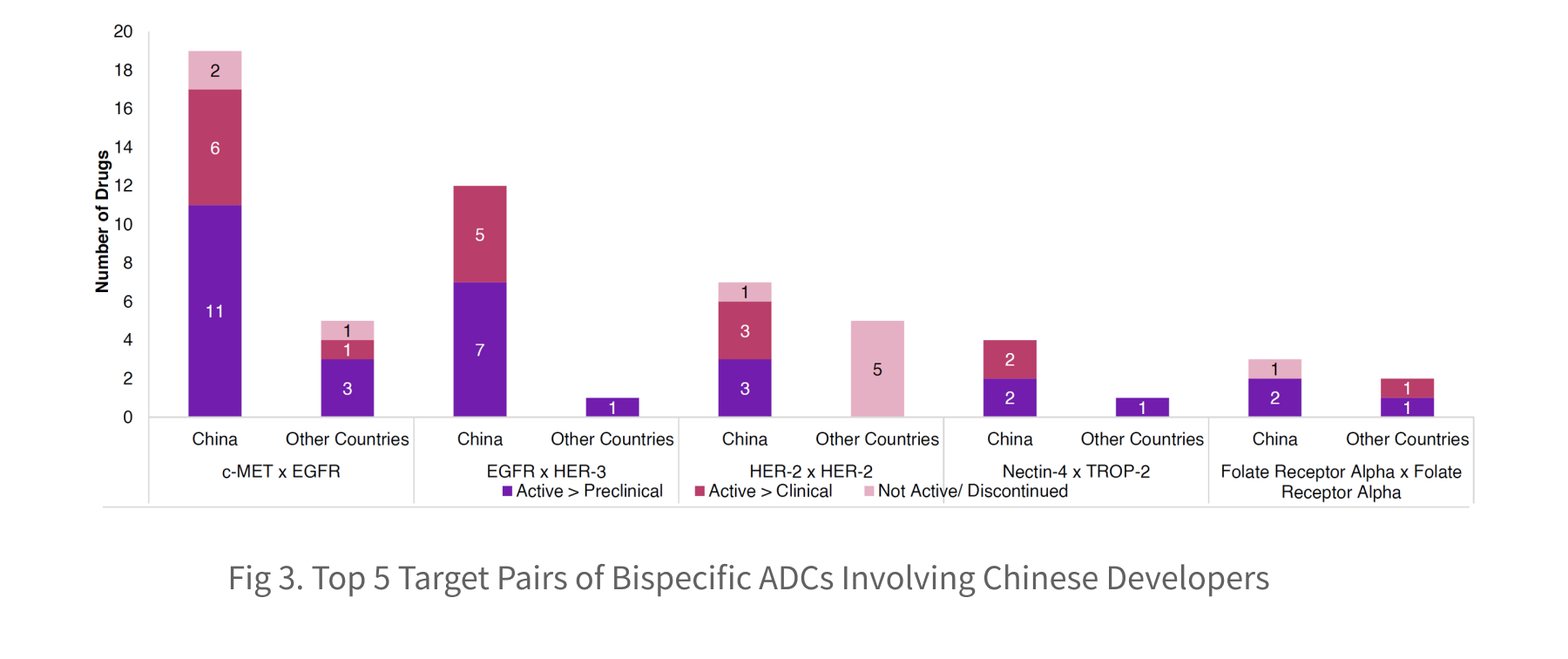

Among bispecific ADCs involving Chinese developers, c-MET × EGFR and EGFR × HER-3 are the two dominant target pairs. Both pairs target pathways frequently co-activated in solid tumors, making them attractive for next-generation ADC design. China has established a position of development leadership in bispecific ADCs targeting c-MET x EGFR and EGFR x HER-3 receptors. Specifically, China-based developers account for 79% (19/24) of all programs targeting c-MET x EGFR and 92% (12/13) of programs targeting EGFR x HER-3, highlighting its near-exclusive focus on these dual-targeting modalities.

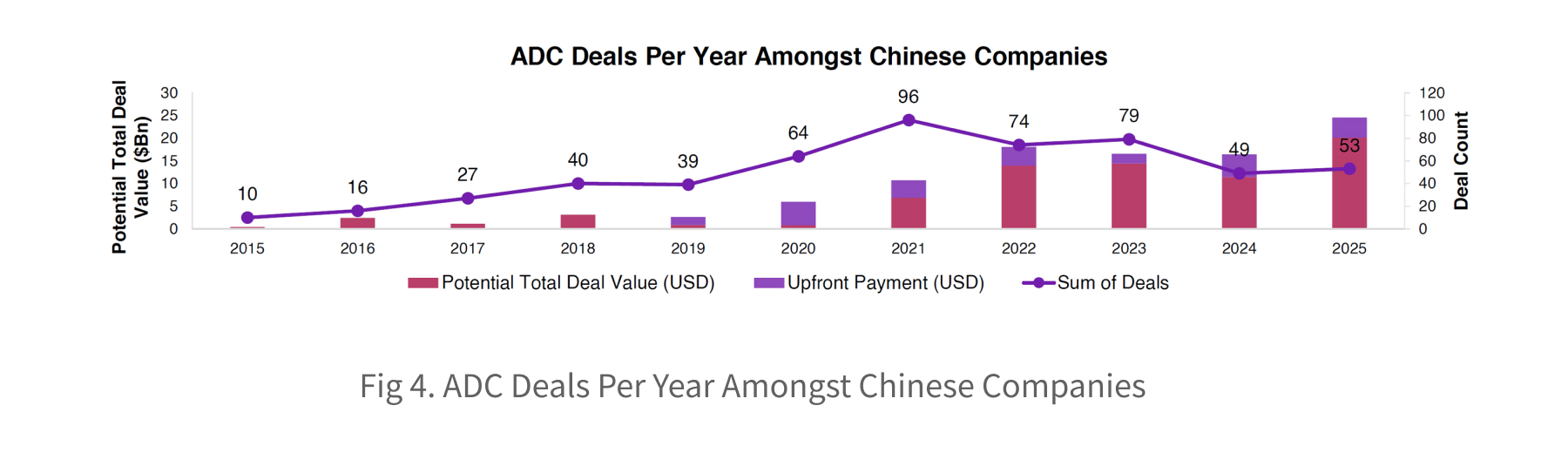

Over the past decade, China has transitioned from being primarily manufacturing-focused to becoming a major investor and developer in ADC innovations. Globally, there are 2,734 ADC deals, with 547 of these involving Chinese companies, representing approximately 20% of the global market. In China, ADC deals have grown at a CAGR of 18% between 2015 and 2025, with an increase of $24 billion in potential deal value.

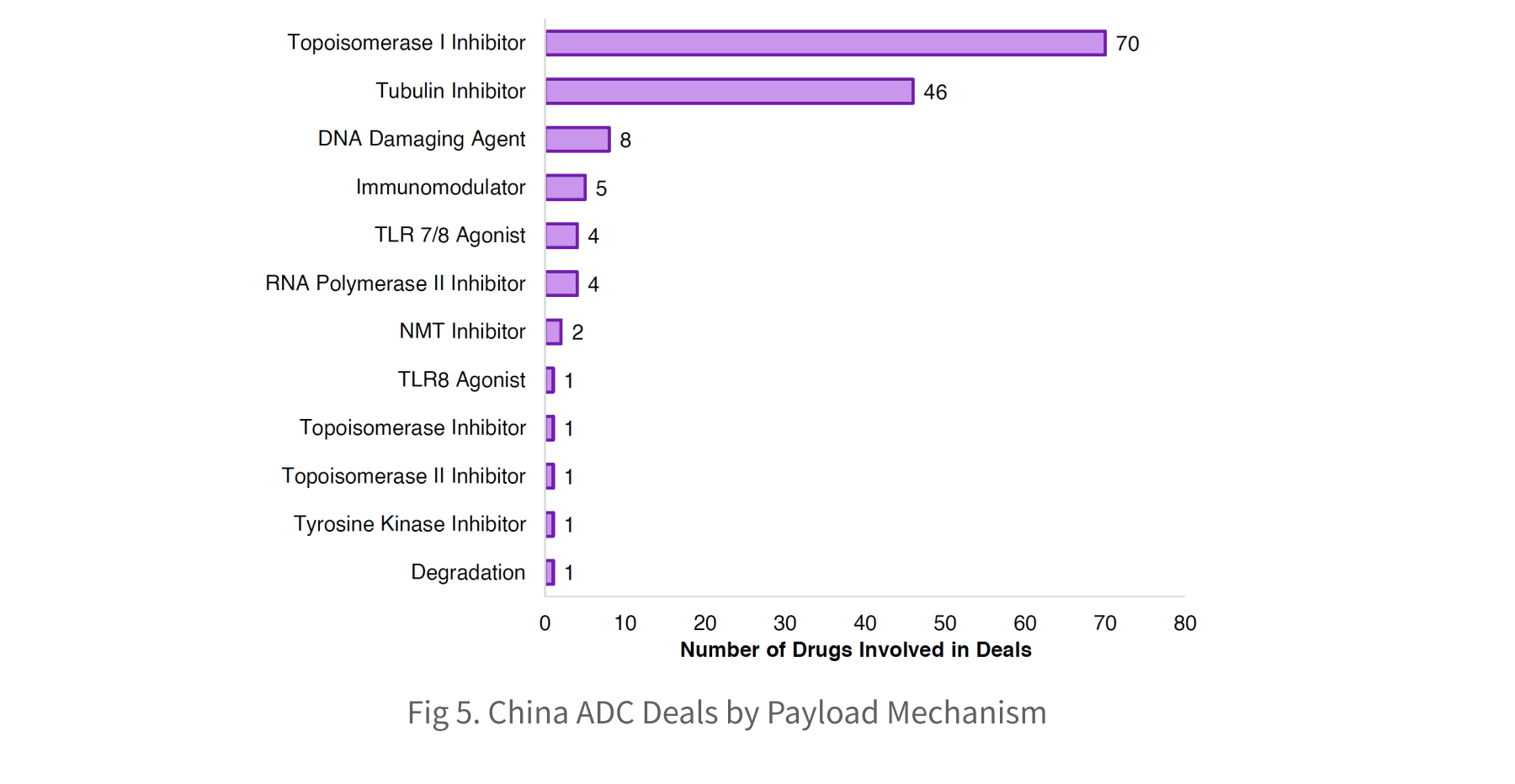

The Chinese ADC deal landscape is increasingly dominated by candidates using topo I inhibitor payloads, which have overtaken tubulin-based approaches. This contrasts with ADC drugs in development, where the converse relationship exists. The number of clinical topo I ADCs has now surpassed tubulin-based assets, signalling that topo I payloads have reached clinical maturity and highlighting their appeal for collaboration and investment. Notable recent deals include the Innovent-Takeda collaboration, and Evopoint Biosciences’ licensing of their traditional ADC to Astellas, valued at up to $1.5bn plus royalties.

Overall, ADCs have become one of the most globally competitive and collaboration-ready therapeutic areas within China’s innovative drug development landscape. In this context, ChemExpress supports the R&D and translation of China-based ADC programs through high-quality payloads, linkers, and integrated one-stop ADC service solutions, facilitating their advancement toward global collaboration.

Interested in Chemexpress service or ADC collaboration opportunities?

Let’s talk! Contact us at:

We look forward to partnering with you to unlock the future of ADC therapies.

Reference:

1.Beacon